Is it a good idea to refinance to a 15-year mortgage? It typically is if you can afford to do so.

Why? Well, to start with, you’ll be free of your mortgage in 15 years, half the time a 30-year refinance would mean.

But, as importantly, you’ll stand to save a serious amount of money. Borrowing large sums over long periods means piles of interest payments. Halving the time you borrow should slash the total cost of your loan.

Nevertheless, 15-year terms mean cramming repayments into 180 months rather than the 360 of a 30-year loan. And that means that each payment will be higher. So, this solution isn’t for those who are already struggling to remain within their household budgets.

In short, refinancing to a 15-year mortgage is usually a good idea if you can afford it.

Key Takeaways

- Even on a fairly average mortgage, you can usually save many tens of thousands of dollars in interest (math below) with a 15-year term.

- You’ll be mortgage-free in 15 years instead of 30.

- Your monthly payments will almost certainly be much higher, meaning 15-year terms are only an option for those with spare cash flow.

Pros and Cons of a 15-Year Mortgage

Here’s a list of pros and cons when you refinance to a 15-year mortgage. We’ll go into more detail for each later in this article.

Pros when you refinance to a 15-year mortgage

- The money you save in the long term on interest could transform your investment and retirement portfolios or fund a better lifestyle.

- You could be mortgage-free in a decade and a half.

- You’ll build equity more quickly with a 15-year loan than a 30-year one. That’s because you pay more principal each month.

- Typically, mortgage rates tend to be lower on 15-year loans than 30-year ones, meaning you stand to save even more in interest.

Cons when you refinance to a 15-year mortgage

- Higher monthly payments are the main drawback to shorter loan terms. You’re cramming repayments into a briefer period rather than spreading them thinly over a longer one.

- You’ll get less tax relief (assuming you itemize your deductions). But only because you’re paying less interest, which is a good thing. Read IRS Publication 936 for details about home mortgage interest deduction.

- Closing costs are expensive. But they apply to all refis, not just those to a 15-year term.

Pro: Long-Term Savings On Interest

This is the main reason people choose a 15-year term. Compared with a 30-year loan, the savings are startling.

You can calculate your potential savings using our refinance calculator. The figures will be rough guides until you get in quotes (“loan estimates”) from multiple lenders and choose your best deal. But the calculator can help you model your options.

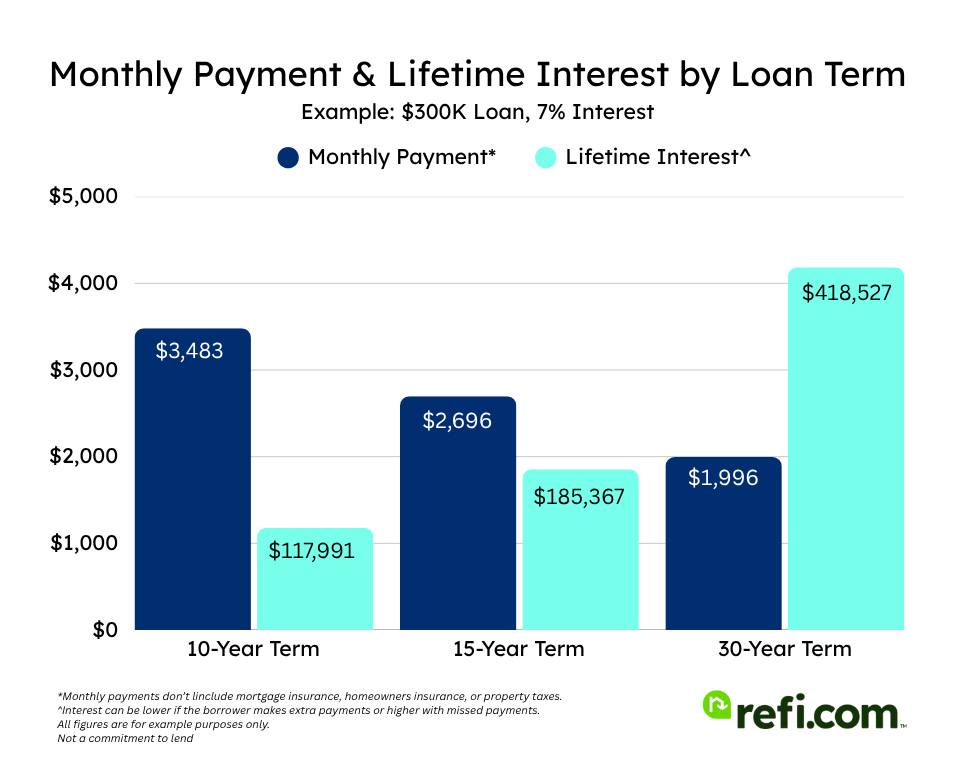

We assumed that your existing 30-year mortgage has a 7.6% rate and has 20 years left. Your home is now worth $400,000 and your current mortgage balance is $300,000. Your monthly payments are currently $2,118, and the total remaining payments you must make total $247,417.

What if you refinance to a new 30-year loan?

If you opt for a 30-year refinance at an example rate of 7.189%, your new monthly payment will nudge down to $2,034. But your total remaining payments will be $432,287.

In effect, you’re spreading your home payments over 40 years (10 on your old loan and 30 on your new one), and that’s going to cost you $184,870 in extra interest compared with leaving your current loan untouched.

“Most people take out a 30-year loan because it keeps their payments lower, with the principal loan balance amortized over 30 years,” explains Mason Whitehead, a Dallas-based branch manager for Churchill Mortgage. “Your amortization schedule, however, is not necessarily a straight line where you take the loan amount divided by 30 years.

It is heavily weighted toward repaying the interest you owe in the early years of the loan, then repaying the principal you owe in the later years of the loan. Consider that, on average, you will pay more toward interest than principal over the first 18 years on a 30-year loan.”

What if you refinance to a 15-year loan?

Now, let’s look at the 15-year scenario. “A 15-year mortgage has a shorter maturity period than a 30-year mortgage,” says Katsiaryna Bardos, chair of the Finance Department at Fairfield University in Fairfield, Connecticut. “Because of the shorter maturity, the total interest paid on a 15-year mortgage is considerably smaller than on a 30-year mortgage.

“This happens because interest is compounded for a much shorter 15-year period. In addition, because of the shorter maturity involved, a 15-year mortgage is viewed to have less default risk by the mortgage lender. As a result, the lender will typically charge a lower mortgage rate.”

Refinancing at an example rate of 6.356% will mean a higher monthly payment: $2,590, which is $472 more than if you left your current mortgage untouched.

But the total payments you must pay over 15 years will be $166,133. That’s $81,284 in savings over leaving your current mortgage in place. And it’s $266,154 less compared with refinancing to a new 30-year mortgage!

Seriously, that’s more than a quarter of a million dollars you stand to save by opting for a 15-year rather than 30-year term.

Your only real question is whether you can afford the closing costs upfront and the extra $472 each month on top of your current mortgage payment.

Pro: Building Equity Faster

When your mortgage starts, you owe a huge amount of money. And you have to pay interest on that amount.

That means a large chunk of your first year’s payments goes on interest and a small proportion goes to reducing your principal balance. In the current mortgage (before refinancing) in our example, $19,633 of your 10th year of payments cover interest while only $5,784 reduces the amount you owe.

Very gradually, the proportion of each payment required for interest as the amount you owe slowly falls. But it’s often 15 or 20 years before you’re paying more principal than interest.

But in our 15-year refinance example, the principal portion of your payment will be bigger than the interest in year 5. And you will have halved your principal balance by year 10.

So, a 15-year mortgage allows you to build your equity — and therefore your net worth — much more quickly than a 30-year term does. And, if you need the funds, you may be able to tap more of your equity with a cash-out refinance, a home equity loan, or a home equity line of credit (HELOC).

Pro: Lower Interest Rates Than Longer-Term Loans

Shorter-term loans typically come with lower interest rates than longer-term ones. But mortgage rates change daily and sometimes more often so check with a lender for current rates.

How we source rates and rate trends

Rates based on market averages as of Mar 24, 2026.Product Rate APR 15-year Fixed Refinance 5.73% 5.77% 30-year Fixed Refinance 6.60% 6.63%

Con: Higher Monthly Payments

The reason everyone doesn’t opt for a 15-year loan is that monthly payments are almost always higher than on a 30-year one. You saw in our example that someone with our imaginary scenario would need to find an extra $472 monthly compared with leaving their current mortgage intact.

If you’re now thinking, “That’s nothing,” then you should explore the idea of refinancing to a 15-year term. You stand to make real gains.

However, if you’re now thinking, “You’re kidding. I’m already stressed out about paying bills,” then you should probably either wait or refinance to a 30-year loan until you have more spare cash flow.

Con: Less tax relief

The less you pay in mortgage interest, the less you’ll be able to deduct from your federal tax bill — assuming you itemize deductions. This isn’t an issue for most borrowers.

After all, you’d probably rather pay less than be able to claim back a proportion of what you pay. And, anyway, most people don’t itemize their deductions.

It’s possible that some, however, have highly complex tax affairs and value this deduction. If so, consult your tax professional for advice.

For a full explanation of the tax implications, read IRS Publication 936 — Home Mortgage Interest Deduction and run your scenario by a licensed tax pro before filing.

Con: Closing Costs

This doesn’t apply especially to 15-year refinances. Whatever the term of your refinance, it will come with closing costs.

And these aren’t cheap. “Refinancing costs can vary, but you can typically expect to pay between 2% and 5% of your loan amount and closing costs,” says Dennis Shirshikov, head of growth at Awning.com and a finance and economics professor at the City University of New York. On a $300,000 refi, that could be anywhere between $6,000 and $15,000.

Lenders often offer special deals that require you to come up with no cash for closing costs. Federal regulator the Consumer Financial Protection Bureau (CFPB) explains:

“There are two ways lenders can do this. One way is by charging you a higher interest rate and giving you a credit to cover the cost of making the loan. The other way is by adding the closing costs to your loan amount. A higher interest rate will mean you pay more over time and a higher loan amount will increase your payments and reduce your equity.”

So, in the long term, you’ll be better off funding closing costs from your savings. But not all of us have that sort of spare cash lying around.

Be aware that some lenders tend to charge higher closing costs alongside lower refinance rates. And others charge lower closing costs alongside higher refinance rates. Shop with both rate and closing costs in mind.

Shortening Your Term vs. Paying Extra Principal

If 15-year rates are higher than your current 30-year rate, you can create your own 15-year mortgage by making larger payments on your existing mortgage.

But timing matters. If you’re early in your loan, refinancing could maximize interest savings. If you’re well into your mortgage, extra principal payments might be a better option since most interest has already been paid—and you’ll avoid closing costs.

If you go the extra principal payments route, just make sure your lender knows to apply all your additional early payments to your principal balance (the amount you owe) rather than across the principal and interest. A call and follow-up letter should achieve that. Many online mortgage portals allow you to specify where your extra contributions go.

Simply use an amortization calculator to find out the required extra monthly payment needed to retire your loan in 15 years.

Related: Strategies For Paying Off Your Mortgage Faster

When It Makes Sense to Refinance to a 15-Year Loan

If you want to reduce your interest bill, it pretty much always makes sense to opt for a 15-year term over a 30-year loan. But only if you can comfortably afford the higher monthly payments.

However, once you’ve made your choice, you have to stick with it. Your lender will expect you to keep up with the payments you signed up for.

“Your monthly payments will be significantly higher than if you had stuck with a 30-year loan. This may pose an issue down the line if any unexpected events impact your income,” cautions Sean Grzebin, head of Consumer Originations at Chase Home Lending. “Your higher monthly costs may not leave room for additional homeownership expenses, such as renovations or unexpected repairs and maintenance.”

And, if life takes a sudden, unexpected turn for the worse, you might have to refinance yet again to get yourself out of trouble with a 30-year mortgage. Unfortunately, that would mean another unpleasant dose of closing costs. If you can qualify for the loan at all.

So, you might want to think twice about a 15-year term if you have health issues that might deteriorate or if your job or industry is less secure than most.

Shopping for a Lender

The CFPB published a paper in May 2023 under the headline, “Mortgage data shows that borrowers could save $100 a month (or more) by choosing cheaper lenders.” That was based on research when mortgage rates were low, so that $100 may be more by now.

The fact is that different lenders charge different rates and closing costs. And, if you pick the wrong one, you could be tens of thousands of dollars down. Remember, $100 a month over 360 monthly payments (30 years) is $36,000.

You probably shop around for the lowest price when buying a car, washer or home cinema. And the stakes with those are typically much lower than $36,000.

So, take a few hours to shop around several lenders. Get quotes from at least three — but this is a case of the more the merrier.

You can start your quote with Refi.com here.